Christian Conrad and Julius Schoelkopf (2025)

MF2-GARCH Toolbox for Matlab

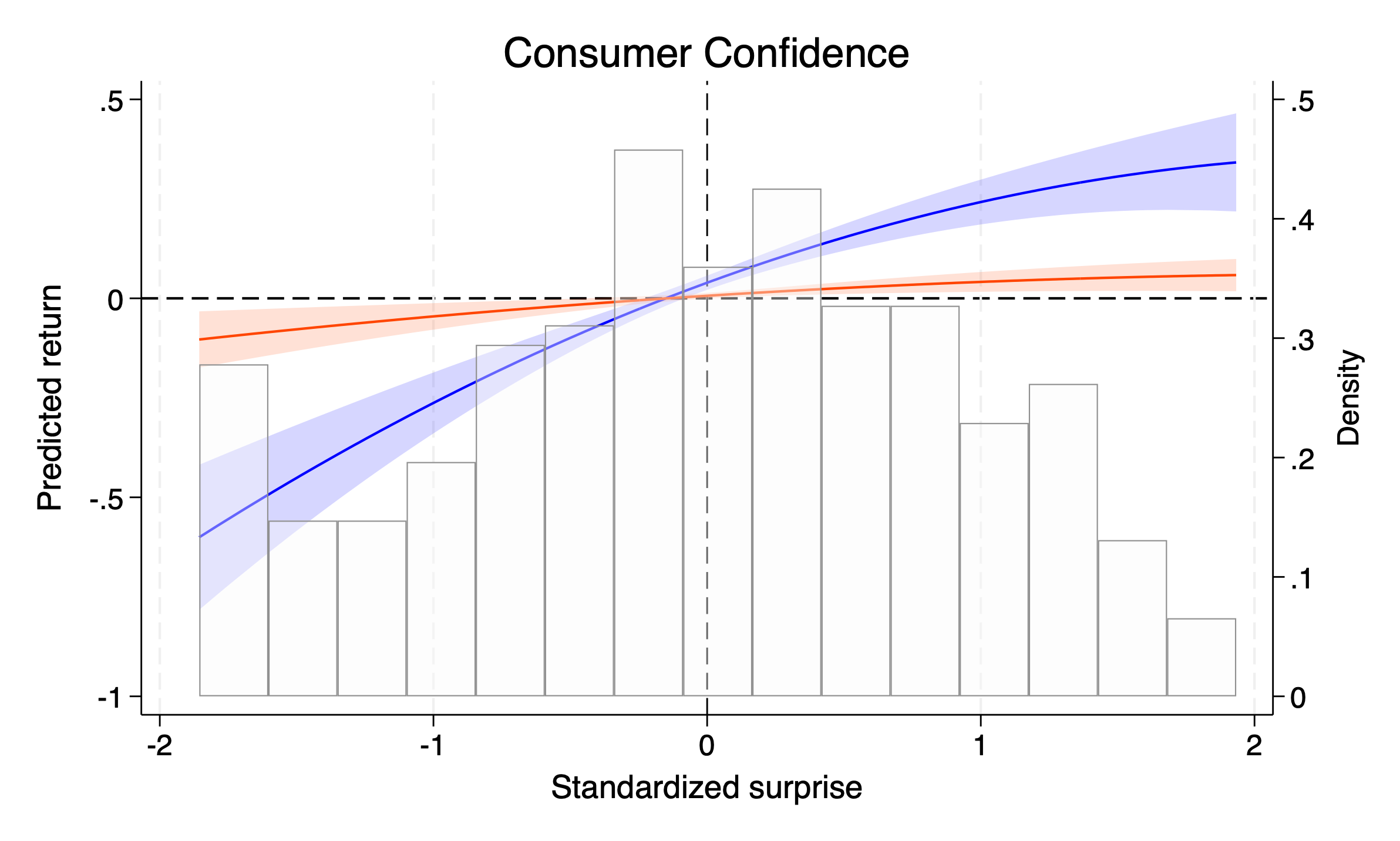

A Matlab package for estimating and forecasting using the multiplicative factor multi-frequency GARCH (MF2-GARCH) as proposed in Conrad & Engle (2025), accompanying the paper Long-term volatility shapes the stock markets sensitivity to news by Conrad, Schoelkopf, and Tushteva (2024).

- A comprehensive toolbox for estimating and forecasting volatility using the MF2-GARCH-rw-m.

- Code for four applications: estimation, news impact curve, out-of-sample forecasting, illustration of forecasting behavior

- You can download the package from its GitHub repository.

- Creator and maintainer

Christian Conrad, Julius Schölkopf and Nikoleta Tushteva (2025)

Replication package „Long-Term Volatility Shapes the Stock Market’s Sensitivity to News“

Replication package for replicating the paper Long-term volatility shapes the stock markets sensitivity to news by Conrad, Schoelkopf, and Tushteva (2025).

- Coming soon!

- You can download the replication package from its GitHub repository.

- Creator and maintainer