My research focuses on Macroeconometrics and Financial Econometrics, especially applying time series methods for business cycle, monetary policy, and financial markets analysis, additionally utilizing micro-level data to address macroeconomic questions – particularly how professional forecasters form their expectations.

Publications

Christian Conrad, Julius Schölkopf and Nikoleta Tushteva (2025+) – Forthcoming in the Journal of Econometrics

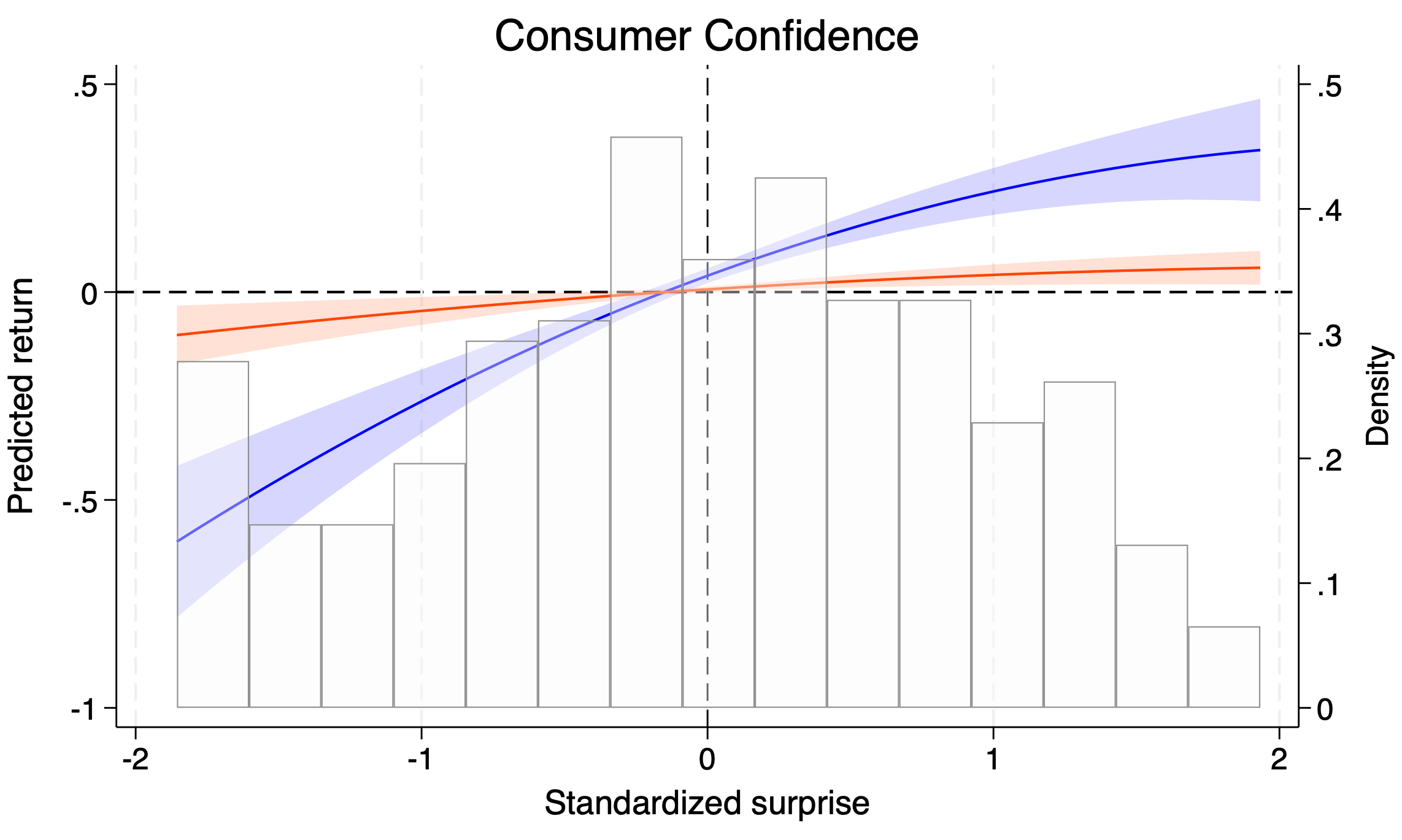

Long-Term Volatility Shapes the Stock Market’s Sensitivity to News

We show that the S&P 500’s instantaneous response to surprises in U.S. macroeconomic announcements depends on the level of long-term stock market volatility. When long-term volatility is high, stock returns are more sensitive to news, and there is a pronounced asymmetry in the response to good and bad news. We explain this by combining the Campbell-Shiller log-linear present value framework with a two-component volatility model for the conditional variance of cash flow news and allowing for volatility feedback. In our model, innovations to the long-term volatility component are the most important driver of discount rate news. Large announcement surprises lead to upward revisions in future required returns, which dampens/amplifies the effect of good/bad news.

Also published in November 2023 as AWI Discussion Paper No. 739, Rimini Cen tre for Economic Analysis Working Paper 23-16, and on SSRN.

Economic Expectations, Survey Data, and Experiments Workshop in Heidelberg (July 2022)*, University of Heidelberg (February 2023, June 2023), University of Sussex (March 2023)*, International Conference for Quantitative Finance and Financial Econometrics at the Aix-Marseille School of Economics (June 2023), Society of Financial Econometrics (SoFiE) European Summer School (June 2023), 10th HKMetrics Workshop in Karlsruhe (July 2023), Econometric Society European Meeting (August 2023), Verein für Socialpolitik Annual Conference (September 2023), Oxford Statistics and Machine Learning in Finance Seminar (November 2023)*, 17th BMRG Conference on Macro and Financial Econometrics (November 2023)*, Workshop on Economic and Financial Forecasting in Karlsruhe (December 2023), 4th HeiTüHo Workshop on International Financial Markets in Tübingen (December 2023), The Society for Nonlinear Dynamics and Econometrics Annual Symposium in Padova (March 2024)*, CIREQ-CMP Econometrics Conference in Honor of Eric Ghysels in Montreal (May 2024)*, Rimini Centre for Economic Analysis International Conference on Economics, Econometrics and Finance at Brunel University London (May 2024), Finance Seminar at the Vrije Universiteit Amsterdam (June, 2024)*, Monetary and Capital Markets Policy Forum at the International Monetary Fund (IMF, July 2024), Macro and Financial Econometrics Workshop, Heidelberg University (Germany, April, Poster), Research Seminar in Banking & Finance of the King’s Business School, King’s College London (November 2025)*.

The * indicates a presentation by a co-author.

Work in progress

Christian Conrad, Julius Schölkopf, Michael Weber and Frank Brückbauer

Beyond the Numbers: Professional Forecasters’ Narratives about Inflation and Stock Market Performance

Professional forecasters‘ heterogeneous narratives through which inflation affects the performance of the stock markets in 2023 rationalizes their high disagreement regarding the quantitative expectations for 12 months ahead inflation and stock returns in December 2022. Professional forecasters causally update their return expectations in heterogeneous directions to information about the inflation outlook depending on their entertained narrative and as well as their asset allocation in a hypothetical portfolio choice experiment. Hence, providing common signals does not necessarily result in a convergence of beliefs if agents subscribe to different narratives.

Working Paper available upon request.

ZEW Mannheim (June 2024), University of Heidelberg (July 2024), 6th Behavioral Macroeconomics Workshop – Heterogeneity and Expectations in Macroeconomics and Finance (organized by IMK, Uni Heidelberg, Uni Bamberg and the Australian National University, July 2024), 11th HKMetrics Workshop (July 2024), ZEW Workshop on Economic Expectations (September 2024*), 7 th Joint Statistical Meeting of the Deutsche Arbeitsgemeinschaft Statistik (DAGStat), Humboldt-Universität zu Berlin (March 2025), 8th Workshop on Subjective Expectations at Nova School of Business and Economics, Lisbon (June 2025), Workshop Heterogenous Macro Expectations – New Evidence and Theory at the Friedrich-Alexander-University Erlangen-Nuremberg (Germany, September 2025), 15th ifo Conference on Macroeconomics and Survey Data, CESifo, München (Germany, October 2025), 6th HeiTüHo Workshop at the University of Hohenheim (Germany, December 2025), 5th IEAP Meeting on Investor Emotions & Asset Pricing (February 2026*), Economics Seminar at University Duisburg-Essen (May 2026*), IAAE Annual Conference at Nova School of Business and Economics, Lisbon (June 2026*), Advances with Field Experiments (AFE) Conference at Becker Friedman Institute for Economics, University of Chicago (September 2026, scheduled), the Banca d’Italia Conference & SUERF Colloquium “Inflation, Inflation Expectations, and Monetary Policy”, Banca d’Italia Rome, Italy (November 2026, scheduled)

The * indicates a presentation by a co-author.

Julius Schölkopf and Muhammed Bulutay

Beliefs and Behavior: Causality in Information Experiments with Cross-Learning

Information provision experiments combined with two-stage least squares (2SLS) identify the causal effect of beliefs on behavior under the assumption that the treatment shifts only the targeted belief. This assumption fails whenever the information also moves other beliefs that matter for the outcome, a phenomenon we label cross-learning. We discuss plausible cross-learning scenarios, analyze what the 2SLS estimator identifies in each case, and show that none of the three standard responses in the literature recovers the structural target under all plausible scenarios. In simulations calibrated to the inflation-spending literature, the cross-learning bias is of the same order as the target effect and can reverse its sign when the unobserved coefficient on the co-updated belief is opposite-signed to the direct effect. Last, we propose recommendations for new survey experiments, which include controlling for co-updated beliefs, multi-arm designs instrumenting several beliefs jointly, bounds from economic restrictions, and eliciting subjective causal models before treatment whenever the respondent population is plausibly heterogeneous in updating type.

Working Paper available upon request.

12th HKMetrics Workshop in Mannheim (June 2025*), Macro- and Financial Econometrics Seminar, Heidelberg University (April 2025*), Advances in Field Experiments 2025 Conference at the University of Chicago (September 2025), Workshop „Theoretical and Experimental Macroeconomics“ at Barcelona Summer Forum (June 2026*)

The * indicates a presentation by a co-author.

Christian Conrad, Zeno Enders, Julius Schölkopf

Heterogeneous Expectation Formation. Evidence from International Forecasts

Using forecasts from professional forecasters for various countries and macroeconomic variables, we study whether deviations from full-information rational expectations are primarily forecaster-specific or process-specific. Our results show that heterogeneity in behavioral bias dominates heterogeneity in the underlying data-generating processes, supporting expectation-formation models with heterogeneous behavioral parameters.

ZEW Workshop on Economic Expectations (September 2024).