Latest news from my blog

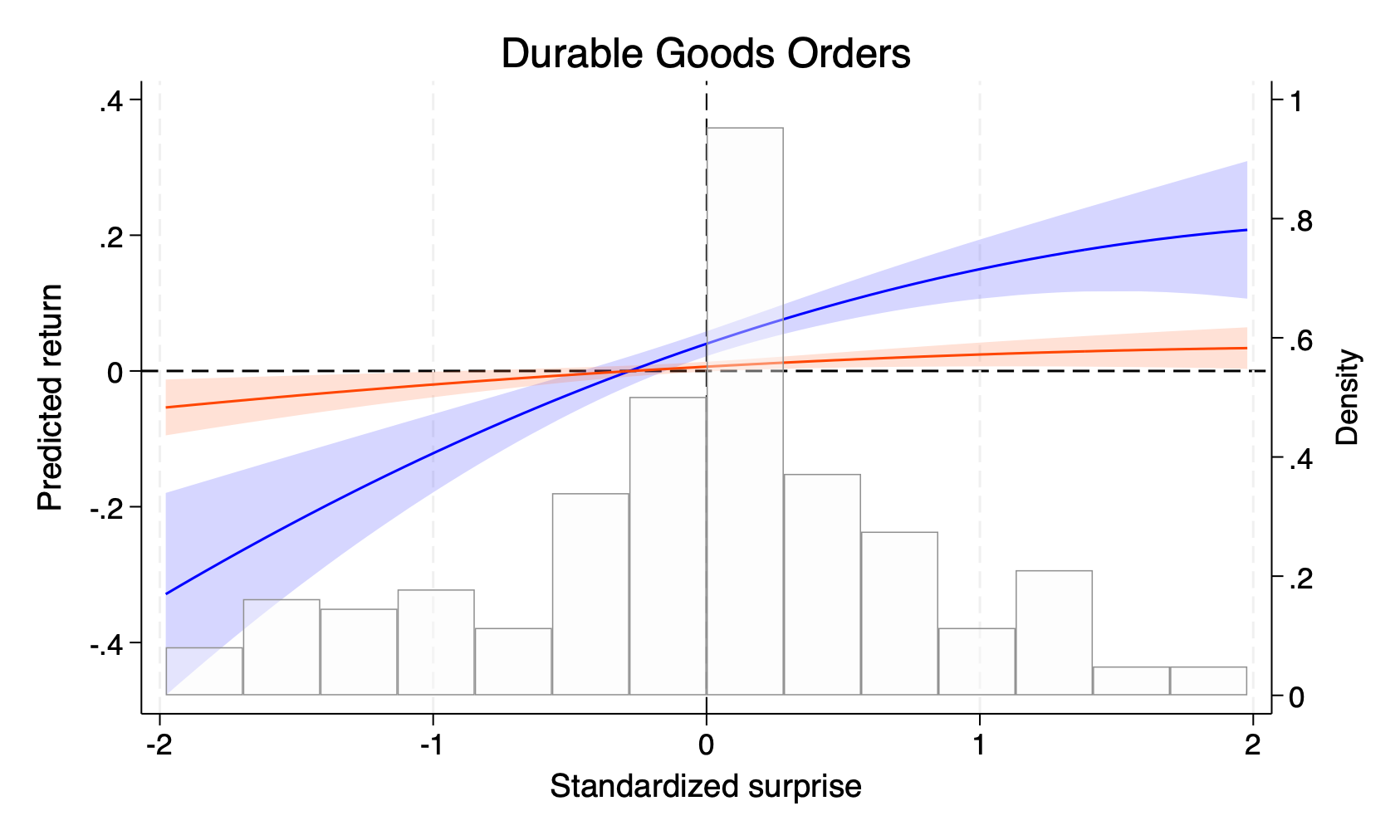

Our paper „Long-Term Volatility Shapes the Stock Market’s Sensitivity to News” (joint with Christian Conrad, Heidelberg University, and Nikoleta Tushteva, European Central Bank) is forthcoming in the prestigious Journal of Econometrics. Macroeconomic announcements are scheduled releases of economic data and indicators by government agencies, for instance, […]

I joined Dan Murphy live on CNBC’s Capital Connection to discuss the macroeconomic situation on Tuesday, March 11, when Wall Street tumbled, as investor concerns over tariffs and recession fears triggered a sell-off. During the interview, I emphasized the importance of resolving tariff and economic policy uncertainty and noted […]

Until November 5th, millions of Americans will head to the polls to choose between two presidential candidates. This decision represents a clear choice between „continuity“ or an „America First“ policy. The campaign of both candidates has focused on how to reduce inflation and new ideas for […]